Consider the drift diffusion equation

$$\dfrac{\partial}{\partial t}\psi=\mu\dfrac{\partial}{\partial x}\psi+\kappa^2\dfrac{\partial^2}{\partial x^2}\psi.$$

Dimensional analysis tells us that $\mu$ is a characteristic length per time (drift velocity) while $\kappa$ is a characteristic length per square root of time. This small factoid has curious consequences.

In statistical physics, $\kappa^2=2D$ is the diffusion coefficient. What follows also applies to non relativistic quantum mechanics, except the diffusion coefficient is imaginary, $\kappa^2=\frac{i\hbar}{2m}$.

Given the value $x(t)$ of a curve/stochastic process at time $t$, for any time interval $\Delta t > 0$, we can test for $x(t+\Delta t)$ and the increment $\Delta x\equiv x(t+\Delta t)-x(t)$ is probabilistic and dependents on $\Delta t$ (and possibly on $t$ or even on $x(t)$).

For example, in the case of a Brownian motion each new $\Delta x$ takes values according to the distribution

$P(\Delta x)=\dfrac{1}{\kappa\sqrt{\Delta t}\sqrt{2\pi}}\exp \left( -\dfrac{1}{2}\dfrac{(\Delta x)^2}{\kappa^2\,\Delta t} \right)$.

(I set $\mu=0$ and note that usually one uses a variable $\sigma=\kappa\sqrt{\Delta t}$)

The Gauss curve distribution for $\Delta x$ says that even for very small $\Delta t$, there is a non-vanishing change that $x(t+\Delta t)$ is far away from $x(t)$. For bigger $\Delta t$, the distribution flattens out and the chance for bigger net deviation grows.

(Sidenote:Note that this weight also arises in the quantization of

$L(q,{\dot q})\propto {\dot q}^2$:

$\frac{(\Delta x)^2}{\Delta t}=\left(\frac{\Delta x}{\Delta t}\right)^2\Delta t\approx \int_0^{\Delta t} \left(\frac{{\mathrm d}x}{{\mathrm d}t}\right)^2{\mathrm d}t$.)

Now, for the above $P$, we have:

$\langle \Delta x\rangle=0$

$\langle \left|\Delta x\right| \rangle=\sqrt{\tfrac{2}{\pi}}\,\kappa\,\sqrt{\Delta t}$

$\langle (\Delta x)^2\rangle=\kappa^2\,\Delta t$

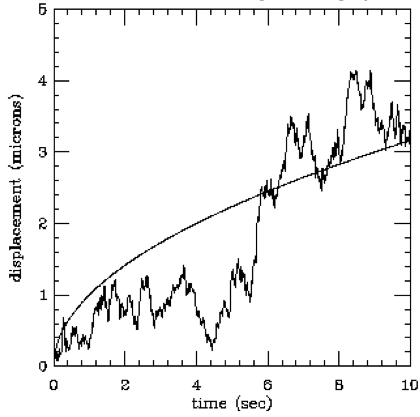

This says that the movement has no preferred direction, but for a finite waiting time $\Delta t$ and if $x(t)$ is some mean path, we expect $x(t+\Delta t)=x(t)+\kappa\sqrt{\Delta t}$, see picture. The intuition is that for a very small waiting time, you could possibly already have a big deviation and the longer the wait the farther you get away from the center - however this movement is sub-linear because with more time, more and more cancellation occur as well. A non-differentiability of the curve in the model manifests itself here: While we know the overall deviation goes as $\sqrt{\Delta t}$, we can't make a good estimate for the instantaneous growth, because at $\Delta t=0$ the slope of the square root function $\frac{∂}{∂\Delta t}\sqrt{\Delta t}\propto\frac{1}{\sqrt{\Delta t}}$ isn’t finite! There is no $x'(t)$!

The accumulation of the values of a function $F$ along a smooth path $x(t)$ is

$\int_{t_0}^{t_1} F(x(s))\, {\mathrm d}x(s)$,

which is

$\int_{t_0}^{t_1} F(x(s))\, x'(s)\, {\mathrm d}s$,

where

$x'(t)=\lim_{\Delta t\to 0}\frac{x(t+\Delta t)-x(t)}{\Delta t}$.

Stochastic integrals are a means of computing the accumulation of a function along a path in cases where the above isn't defined. An Itō process is a stochastic process $X_t$ which is the sums of a Lebesgue and an Itō integral:

$X_t = X_0 + \int_0^t \mu_s(X_s, s)\,\mathrm ds + \int_0^t \sigma_s(X_s, s) \,\mathrm dW_s$

An Itō integral is roughly a Riemann integral of random variables. The norm in which the limit of partial sums converges is not the norm on $\mathbb R$, but instead the result is defined as a random variable for which the probability of being different than the limit goes to zero.

One writes

${\mathrm d}X_t = \mu_t(X_s, s) \, {\mathrm d}t + \sigma_t(X_s, s) \, {\mathrm d}W_t$

for the integral above. If $X_t$ isn't known, this is called a stochastic differential equation in $X_t$.

Being an Itō process is the stochastic analog of being differentiable.

If $\mu_t$ and $B_t$ are time independent, we speak of Itō diffusion. A geometric Brownian motion is characterized via $\mu_t(X_s, s)=X_s\,\mu$ and $\sigma_t(X_s, s)=X_s\,\sigma$, i.e. both are "just" $\propto X_s$.

The famous Itō lemma is

${\mathrm d}f(t,X_t) = \left(\dfrac{\partial f}{\partial t} + \dfrac{\sigma_t^2}{2}\dfrac{\partial^2f}{\partial x^2}\right){\mathrm d}t + \dfrac{\partial f}{\partial x}\,{\mathrm d}X_t$

The second derivative term comes from stochastic diffusion, a non-local flavor if you will.

As this really is an integral relation, it corresponds to a version of the fundamental theorem of calculus. If we know how to integrate against $X_t$, we can compute $f(t,X_t)$ as such an integral (plus an ordinary integral).

Note that for $f(x,t)=\frac{1}{2}x^2$ and $\frac{\sigma_t^2}{2}=\kappa^2$ we get

${\mathrm d}\left(\frac{m}{2}X_t^2\right) = m\,\kappa^2{\mathrm d}t + X_t\,m\,{\mathrm d}X_t$

The next part is on the commutation relations $xp$ minus $px$, a version of the last equation which characterizes $x$ in the second term $px$ as detecting a diffusion effect. That's basically part of what Maimon writes about on the Wikipedia page on the path integral formulation of (quantum) mechanics:

Let

$p_{\Delta t}(t)=m\frac{x(t+{\Delta t})-x(t)}{{\Delta t}}$

If the limit

$\lim_{\Delta t\to 0}p_{\Delta t}(t)$ exists, then for axillary

$\delta$, we have $\lim_{\Delta t\to}x(t+\delta^2{\Delta t})=x(t)$.

Hence, for ever smaller time grid size ${\Delta t}$, e.g. an expression like

$x(t+\delta_1^2{\Delta t})\,x(t+\delta_2^2{\Delta t})\,x(t+\delta_3^2{\Delta t})$

converges to $x(t)^3$.

However, for

$x(t+\Delta t)\approx x(t)+\kappa{\sqrt{\Delta t}}$

with the square root, we find

$x(t+\delta^2{\Delta t})\,p_{\Delta t}(t)=\delta^2\,m\,\kappa^2+x(t)\,p_{\Delta t}(t)$.

The result says that two naively equivalent approximation schemes (e.g. $\delta=0$ vs. $\delta=1$) systematically differ by an additive diffusion term (e.g. $m\kappa^2$ here). In quantum mechanics, that's $m\kappa^2=m\frac{i\hbar}{2m}=\frac{i\hbar}{2}$.

So we had

$\frac{\partial}{\partial t} \psi = \kappa^2 \frac{\partial^2}{\partial x^2} \psi$

(note the imbalance of dimensions, $t$ vs. $x^2$) and in turn

$P(\Delta x) \propto \exp\left(c\frac{(\Delta x)^2}{\Delta t}\right)$

as next-step distribution, and then

$\langle |\Delta x|\rangle\propto (\Delta t)^{1/2}$

gives the non-smooth curve.

You may want to look at other next-step distributions,

effectively giving the theories with $\langle |\Delta x|\rangle\propto (\Delta t)^{1/\alpha}$. We can see that the proportionality coefficient (the analog of $\kappa$ or the velocity) must be fractional and in turn we expect a fractional differential operator $\frac{\partial^\alpha}{\partial x^\alpha}$ in the corresponding diffusion equation. You get a Laplacian to the power of $\frac{\alpha}{2}$. The $\alpha\neq 2$-deformed theory with complex $\kappa$ is what's termed „fractional quantum mechanics“, though I don't know of really notable results, besides better understanding of the known cases.

To answer your question, associate the power of the operators to the above expectation value $\langle |\Delta x|\rangle$. The $\alpha$ it characterizes fast the system parameter in your model stochastically moves away from the center. So called Levy-flights might propagate in a rough way, the current/velocity becomes something more complicated (not proportional to the momentum, i.e. the thing that gets multiplied by $x$ in the plane wave solution). The Brownian normal-derivative case is friendliest diffusion. You wouldn't gain that intuition from that other question on fractional derivatives, because there the guy cooks up an equation with a fractional derivative of time and we're used to see all of space but only one time (the now).